The Market Party Continues

By Angelo Meda, Head of Equities at Banor

Sell in June and go away

In May, we saw eight consecutive days of stock market gains, a trend that has not yet been interrupted, and we have now entered the ninth consecutive week with positive indices. Anyone hoping for a pause after the strong gains of recent months would have been disappointed: the market politely replied with a resounding “not yet.” Even in recent days, investors have continued to buy equities with a conviction that, in some ways, resembles tourists booking a weekend getaway without even checking the weather.

Technology remains the star, artificial intelligence is centre stage, and indices are close to historic highs. The Nasdaq continues to behave like the model student of the class, while the S&P 500 follows closely behind, supported by earnings growth that, for now, justifies much of investors’ enthusiasm. The real question among market participants is always the same: how long can this last? For the moment, the market’s answer seems to be “longer than we think.”

For a while, every quarterly earnings call of listed companies revolved around buzzwords such as cloud, digital, or metaverse. Today, there is only one magic word: artificial intelligence. Any company even loosely connected to chips, data centres, software, or digital infrastructure is being watched very closely. Every time a company reports better-than-expected results, the market interprets it as yet another confirmation that the major investment cycle linked to AI is still in its early stages.

It’s a bit like watching a party that keeps attracting new guests: as long as new people keep arriving, no one really thinks about going home.

Of course, valuations for some stocks have reached significant levels, and it would be naive to think the path can always be linear. However, so far earnings are growing fast enough to allow investors to sleep relatively soundly.

Meanwhile, the Federal Reserve continues to play the role of the neighbour everyone watches from their window: every economic data point is analysed in detail in hopes of understanding the central bank’s next move. Inflation continues to show signs of moderation, but not enough for central bankers to declare the battle definitively over. This week, labour market data will be released, and any possible outcome seems positive. If job creation slows, the prevailing view will be that the fight against inflation is nearing completion; if growth continues, the positive interpretation of full employment will dominate. If the expected 85,000 new jobs are confirmed, it would create an ideal scenario of stable unemployment near its lows and trends that could persist.

For now, the market seems to have found an almost perfect balance: sufficient economic growth to support earnings, but not so strong as to reignite inflation fears. A delicate balance, yet surprisingly resilient.

On one hand, Wall Street confirms itself as the “rock star of the world tour,” while Europe plays the role of the reliable musician who rarely makes the cover but always performs well. European markets have participated in the global rally, supported by generally encouraging corporate results and a European Central Bank increasingly inclined toward a gradual easing of monetary conditions. The Italian stock market continues to deliver strong results. After years of trailing other international exchanges, Italy now finds itself in a much more interesting position, supported by solid banks, competitive industrial companies, and still reasonable valuations. It may not be the loudest market, but that is often its strength.

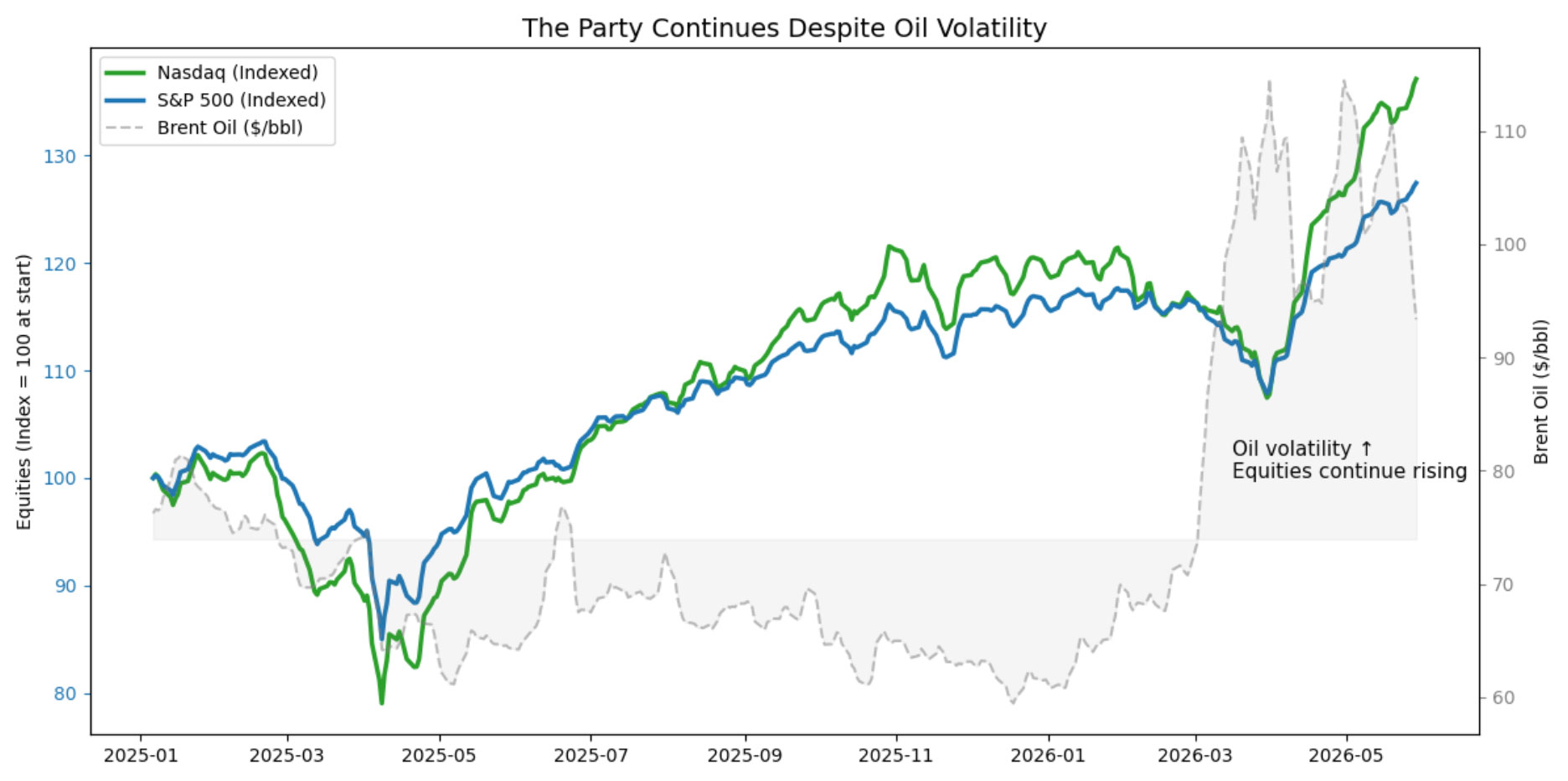

Geopolitical tensions have brought some volatility back to the energy market, and oil has shown signs of awakening. Whenever crude rises sharply, investors immediately begin to question the potential impact on inflation. For now, however, market reaction has been almost indifferent, as shown in Figure 1. It is as if investors have decided that, as long as earnings continue to grow and the global economy shows no clear signs of slowing, some geopolitical tension can be tolerated without too much drama—further evidence of how constructive sentiment remains.

Figure 1: Rising oil volatility has not disrupted the upward trajectory of equity markets, underscoring the resilience of the current rally.

And now?

Looking ahead, the outlook remains favourable but not without risks. On one side, we have companies generating solid profits, still-resilient consumers, and a technological revolution that fuels enthusiasm and investment. On the other, we see elevated valuations, very ambitious expectations, and markets that seem to have already priced in a lot of good news. In other words, the bull market continues its run, but is beginning to show signs of fatigue. For investors, this does not necessarily mean turning pessimistic, but rather remembering that even in the strongest bull markets there are pauses, profit-taking phases, and sudden returns of volatility (not to mention that within indices there are many stocks, and they do not always move in unison).

That said, the feeling is that the market has not yet exhausted its energy. Artificial intelligence remains the main fuel, liquidity is still abundant, and central banks, while cautious, do not seem inclined to hinder growth.

In short, the past week has reinforced a simple message: markets continue to see the glass as half full—perhaps even more than half. For now, no one seems in any particular hurry to remember where the exit to the party is.

This document has been prepared by the investment manager of the SICAV, Banor Capital Ltd., a company authorised and regulated by the Financial Conduct Authority (FCA). The content is for information purposes only and does not constitute investment advice, a recommendation, or an offer/solicitation to buy or sell any investment. Views are those of the speaker and may change. Any views expressed regarding future market conditions, sector performance, or investment returns are forward-looking statements and may not materialise. Actual outcomes may differ materially. Forecasts are not a reliable indicator of future performance. This communication is not directed to any person in any jurisdiction where doing so would be unlawful; distribution may be restricted.

Angelo Meda is Head of Equities at Banor SIM S.p.A. and provides research and advisory input to Banor Capital Ltd pursuant to an advisory agreement.

This article is an English translation of an article originally prepared and published by Banor SIM.